showCASE No. 120: Resilience of remittance flows to the Southern Neighbourhood countries

Editorial

Remittance flows throughout 2020 and the first six months of 2021 have for the most part proven to be much more resilient than it was initially feared.

In this edition of showCASE, we explore how the value and importance of money send by diasporas to the countries in the EU’s Southern Neighbourhood evolved amid the Covid-19 pandemic. As we argue, the pandemic period provided a valuable lesson on what could be done in the future to further facilitate remittance flows.

-----------------------------------------------------------------

CASE Analysis

Written by: Katarzyna W. Sidło

Money transferred by migrants to families and friends back in their home countries, otherwise known as remittances, have long been perceived as one of the “most direct and well-known links between migration and development”. Indeed, beyond being an important instrument in alleviating poverty in the recipient countries, they benefit entire economies. Much concern was therefore expressed regarding the effect that the global health crisis might have on the remittance flows at the beginning of the Covid-19 pandemic, both globally and in the countries in the European Union’s (EU’s) Southern Neighbourhood (SN).[1]

In that sense, the pandemic has provided a valuable lesson on what could be done in the future to further facilitate remittance flows.

Remittances as a lifeline

The positive link between remittance flows and economic growth, consumption, and investment in recipient countries has been proven by numerous studies (although admittedly some researchers argue that remittance flows disincentivize local labour market participation). Money received from relatives and friends abroad help struggling households to meet their basic needs. Indeed, according to the World Bank, three out of every four dollars received by the recipient households are used to “put food on the table, cover medical expenses, school fees, housing expenses, cover loss of crops, or family emergencies”. Numerous developing countries are thus reliant on the remittance flows that amounted to more than 10% of GDP for 32 countries and more than 5% of GDP for 61 countries globally in 2019. In the SN, money sent from the diasporas have been historically important everywhere but in Algeria and Israel; in fact, in 2019 both Palestine and Lebanon were among the twenty most remittance-reliant economies in the world.

Expected and actual impact of the Covid-19 pandemic

Back in April 2020, the World Bank (WB) warned of the “sharpest decline of remittances in recent history”, which it estimated to amount to about 20% that year. For the MENA[2] region specifically, a drop by 19.6% y/y was expected with a predicted slow recovery by approximately 1.6% y/y in 2021 (against an expected 5.6% y/y growth that year for the low and middle-income countries [LMICs] globally). As the pandemic unfolded, these predictions were revised up, with a new forecast of 7% y/y drop globally and 8% y/y in the MENA region in 2020.

However, it appears that even those revisions were too pessimistic and remittance flows have been much more resilient than expected. In fact, according to the latest numbers released by the WB, in 2020 they declined by just 1.6% y/y. In the MENA region, a growth by 2.3% y/y on average was observed and, in a subgroup comprising of countries in the SN, the year-on-year growth amounted to 2.9%[3]. This is worse performance than in case of Latin America and the Caribbean (6.5% y/y) or South Asia (5.2% y/y) but better than in other parts of the world where inflows declined (although still by less than prognosed at the beginning of 2020).

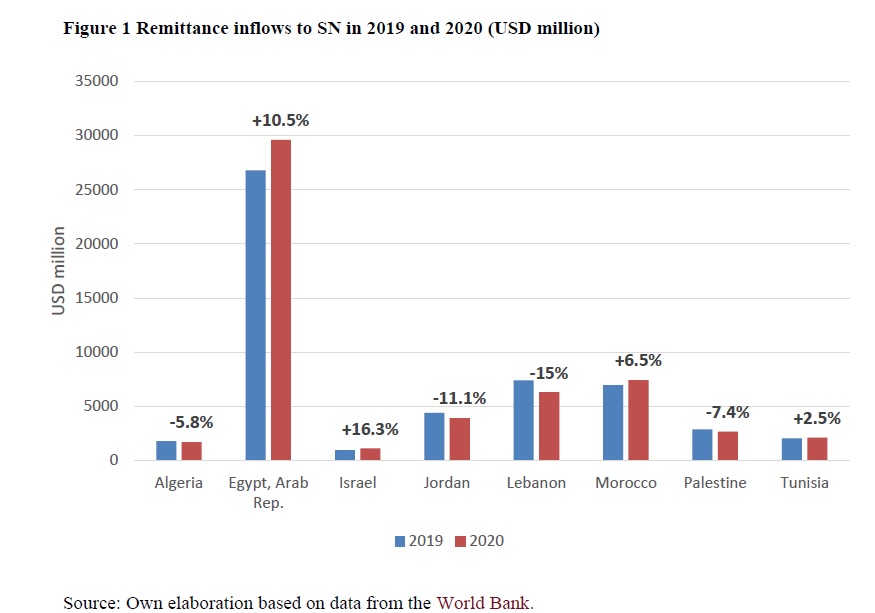

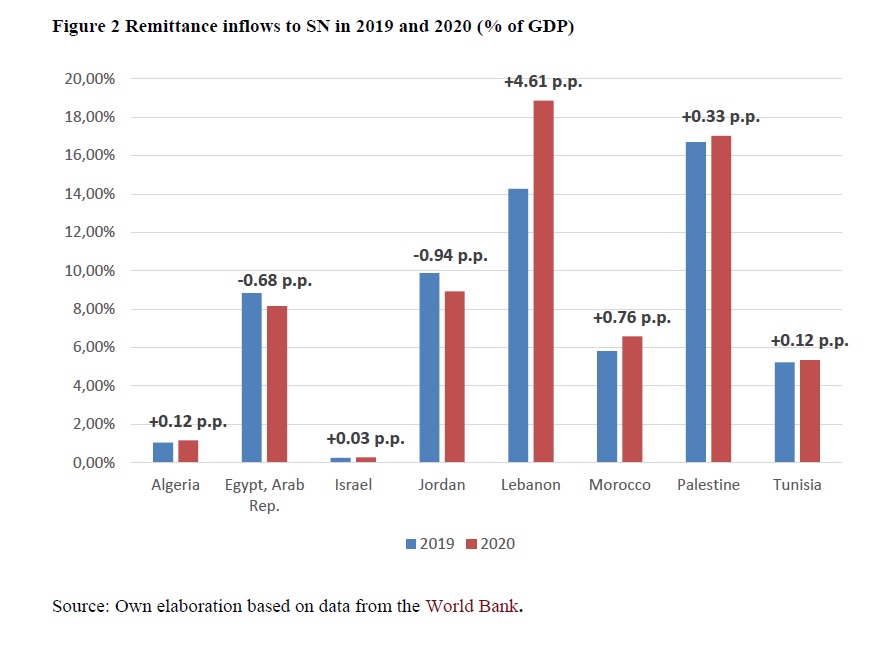

Admittedly, the situation in the SN region has by no means been homogenous (see Figure 1). Most significant increases in the remittance flows occurred in Israel (16.3% y/y) and Egypt (10.5% y/y), with smaller rise observed also in Morocco (6.5% y/y) and Tunisia (2.5% y/y). In contrast, the value of remittance flows (in USD terms) to Algeria, Jordan, Lebanon and Palestine decreased between 2019 and 2020.

In Israel, remittance inflow represented a marginal 0.28% of GDP. Likewise, in Algeria the 6% drop in the remittance inflow was perhaps not greatly noticeable since the remittances amounted to just above 1% of GDP.

In Egypt, on the other hand, the record USD 29.6 billion that were received by the country amounted to 8.15% of the GDP. This is

a significant number, although smaller than in the previous years, which indicates that the nominal GDP growth outpaced that of the remittance flows in 2020 (in fact, Egypt was the only country in the group that experienced growth last year). The opposite was true in Palestine, where the nominal value of the remittances decreased between 2019 and 2020, but their importance for the economy still grew by a margin.

In Morocco and Tunisia, in turn, the value of remittances received in 2020 increased both in nominal terms and relative to GDP. Jordanian economy, to the contrary, saw a decrease both in terms of value of remittances and their proportion to GDP (by 11.1% and 0.94 p.p. respectively).

Arguably, nowhere has the situation deteriorated more than in Lebanon, which even before the outbreak of the pandemic suffered from the pre-existing economic and financial crisis that was further exacerbated by the blast in the port of Beirut in August 2020. Indeed, in 2020, the country saw a drop in remittances by 15% y/y or USD 1.1 billion. In a conspicuous display of the severity of the crisis (the Lebanese economy contracted by 20.3% between 2019 and 2020), the proportion of remittances to GDP increased from 14.3% to 18.9% between 2019 and 2020 which meant that Lebanon surpassed Palestine on the list of world’s most remittances-dependent economies. While undoubtedly those official figures do not paint the whole picture as they do not account for informal transfers and may exclude money sent e.g. via mobile phones[4], they are sufficient to underscore the severity of the situation in the country.

Performance in 2021 thus far

In Jordan, a small but positive change was observed during the first half of the year, with the value of remittances having risen by 0.2% compared to the same period in 2020 (and a reported 100% increase in remittances sent from of the country’s top sources, Qatar, during the same period of time). In Morocco, the first half of 2021 saw a reported 48.1% y/y growth, with remittance flows amounting to approximately USD 3.34 billion. In Egypt, in turn, only a small decline of 0.2% during the first quarter of 2021 (y/y) was noted, whereby remittances went down from USD 7.87 billion to USD 7.85 billion.

Resilience factors

One of the key reasons for the resilience of the remittance inflows was better than anticipated economic performance of the source countries (predominantly France and Italy alongside other EU27 states and the GCC), although their policies towards migrant workers, as well as characteristics of the diasporas themselves, had a significant impact as well. Equally, if not more importantly, the feeling of responsibility for the wellbeing of families and friends back home must have played a part. As both foreign direct investment (FDI) and overseas development assistance (ODA) declined in 2020 – in fact, the World Bank stressed that in 2020 the sum of remittances send to LMICs exceeded both that of FDI and ODA that year – and as tourism receipts dropped exponentially, money sent by the diasporas provided a lifeline for economies back home.

Stumbling blocks

Despite the fact that the pandemic has dominated the news throughout the better part of the last year and a half, multiple other factors were at play in the SN throughout the past year and a half as well.

Crucially, in Lebanon, the political, economic and financial crisis of such severity that it earned itself a dubious honour of being named “in the top 10, possibly top 3, most severe crises episodes globally since the mid-nineteenth century”, hampered the normal functioning in the country, including ability to receive remittances from relatives and friends living abroad. As the international transfers are mostly blocked and bank accounts frozen, the Lebanese are reportedly turning towards cryptocurrencies. This solution has its own limitations, however, not least due to high volatility of the digital currencies.

Inability to transfer money proved a problem throughout the pandemic in Palestine as well. As inward remittances are normally paid in cash and digital payments system is effectively non-existent, transfers were severely impeded amid lockdowns and limitations imposed on mobility of workers.

Throughout the region, the persistently high cost of sending the remittances (amounting to 6.6% of the value of the transfer on average in the last quarter of 2020) remains an obstacle as well. This is true especially for transfers made from the high-income OECD countries, with the cost of sending money from the Gulf Cooperation Council (GCC) more manageable at approximately 3% of

the value of the transaction.

Room for improvement and outlook for the future

The most recent forecast by the World Bank predicts a 2.6% y-o-y increase in remittance flows to the MENA region in 2021. Whether this number proves an underestimation again depends on a number of factors. Indeed, the value of transfers in 2020 could have arguably been even higher had it not been for the obstacles outlined above. This may serve as a valuable lesson for 2021 (and beyond).

Given the significance of the remittances to the economies in the majority of the countries under analysis, it is in the best interest of the governments to do their most to assist with these processes, especially since the pandemic appears to be far from over.

Read / Download the full issue of showCASE

[1] Algeria, Egypt, Israel, Jordan, Lebanon, Morocco, Palestine (as listed by the EU under understanding that this designation shall not be construed as recognition of a State of Palestine and is without prejudice to the individual positions of the Member States on this issue), and Tunisia. No reliable data for Libya and Syria was available.

[2] Covering SN countries as well as GCC (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and United Arab Emirates), Djibouti, Iran, Iraq, and Yemen.

[3] All calculations, unless indicated otherwise, are based on data by World Bank.

[4] For more information on how remittances are defined and estimated,

see https://www.migrationdataportal.org/themes/remittances