CASE tax workshop: The structure and effectiveness of the Polish tax system

An economics workshop devoted to the effectiveness of the Polish tax system was held in Warsaw on Marth 26-27. The organizers were the European Commission; CASE – the Center for Social and Economic Research; Lazarski University; and CenEA, the Centre for Economic Analysis.

The main goal of the workshop was to build connections among Polish economists and to review their current research. The event was also the first stage of a large economic research project to analyze the effectiveness of the Polish tax system. The discussion of the economic aspects of the system of tax rates is intended to raise the level of the debate over taxes, as tax changes are often introduced in a manner that is completely divorced from optimal taxation theory, and are not preceded by economic analysis of existing conditions. Still, the purpose of the project is not to create a vision of the optimal tax system, but only to demonstrate certain tools and provide analysis.

The workshop was preceded by a two-hour panel discussion on the economics of diversified VAT rates, moderated by Marek Chądzyński of the daily newspaper Dziennik Gazeta Prawna. This subject fits with one of the recommendations of the Country report for Poland, which Bartłomiej Wiczewski of the European Commission discussed during the introduction.

Paweł Gruza, a deputy finance minister, took a skeptical view of the idea of a single VAT rate He believes it would be difficult to explain to the voters that it’s fair to have the same rate on a loaf of bread and on an expensive watch. However, he admitted that diversification of rates also imposes significant costs on the administration and taxpayers, and that the current system, in which the Central Statistical Office determines rates based on its PKWiU nomenclature system, creates many problems both for the state and for taxpayers. According to Gruza, some of the problems will disappear when CN codes become the basis for classification. Today there are 220 products and services that cause difficulties in classification.

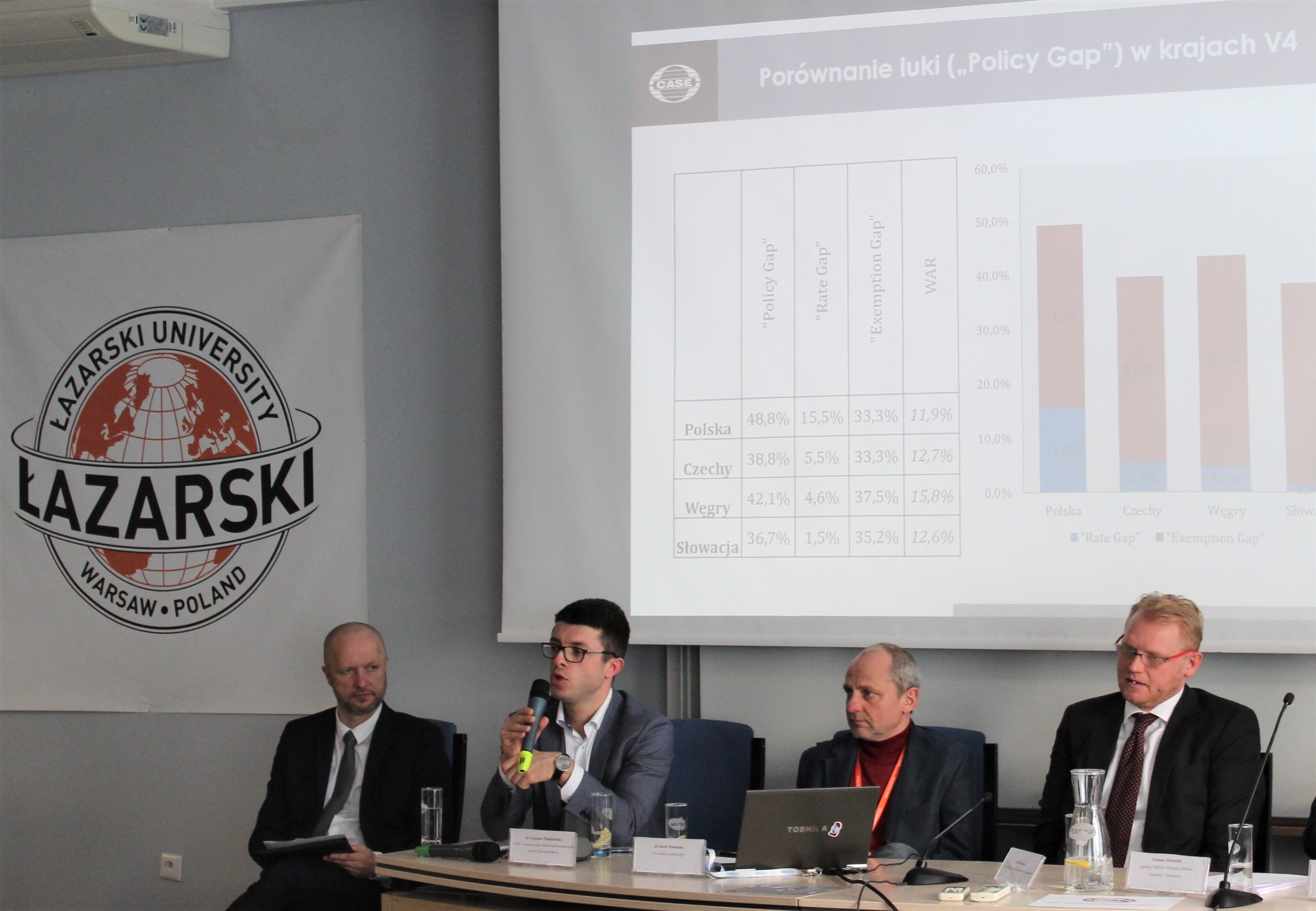

Dr. Grzegorz Poniatowski, director for fiscal policy at CASE, who for many years has been commissioned by the EU to calculate the VAT gap, discussed which groups of products and services with reduced VAT rates have the greatest impact on loss of tax revenue. He compared this to the tax systems of other countries of the region, where reduced rates are used much more rarely. In Poland the loss of revenues related to the application of reduced rates is the highest – another reason why the Commission recommends reducing their use.

Next, Tomasz Michalik of the consulting firm MDDP discussed the Commission’s proposal for liberalization of the rules for setting VAT rates. He also showed how the planned system for VAT settlement in intra-community transactions will look.

Later on in the panel Dr. Jarek Neneman, a lecturer at Lazarski University and a three-time former deputy finance minister, presented the theoretical arguments for diversified VAT rates, toward which he had a generally critical view. Still, he pointed out that a unified VAT rate also has its own negative consequences, other than the universally known regressivity of VAT. “A cool economic analysis of the costs and benefits seems to show unequivocally that from the point of view of effectiveness, unification of rates is a good solution, and when it is bolstered by tools that increase progressivity, it is also beneficial from the social point of view. Still, at the moment in Poland, and more broadly in Europe, there is no appetite for unification of VAT rates, though of course maintaining the 5% and 8% rates makes no sense at all.” He also presented the areas where diversified rates generate costs for taxpayers, for the state and for society: the costs of court proceedings, inspections, advisory services, legal interpretations etc.

Finally, Dr. hab. Michał Myck of CenEA, the Centre for Economic Analysis, presented the results of research on the distribution of the VAT burden on households, showing what benefits society receives from maintaining the costly system of diversified VAT rates. If we compare the value of VAT paid by households to their income, we see high regressivity: the very high share of VAT in the first decile is surprising, but it results from the lack of income, or, negative income, of some households in this group. To a high degree this is a result of the lack of research methods and the known fact that the deciles at each end of the scale are the least representative in this kind of research. A better reference point than household income is household spending, though here too the regressivity of VAT can be seen. The research presented by Dr. Myck was based on data from 2015, and thus did not include family income from the government’s 500+ program.